SMB Market Update for Q1 2026

As noted in our SMB Advisory year-in-review remarks, following a slowdown in new transaction activity in mid-2025, M&A activity in the Canadian private company market has picked up. We’re observing an increase in business owners initiating pre-sale planning, alongside sustained demand from both strategic and financial acquirors for high quality companies.

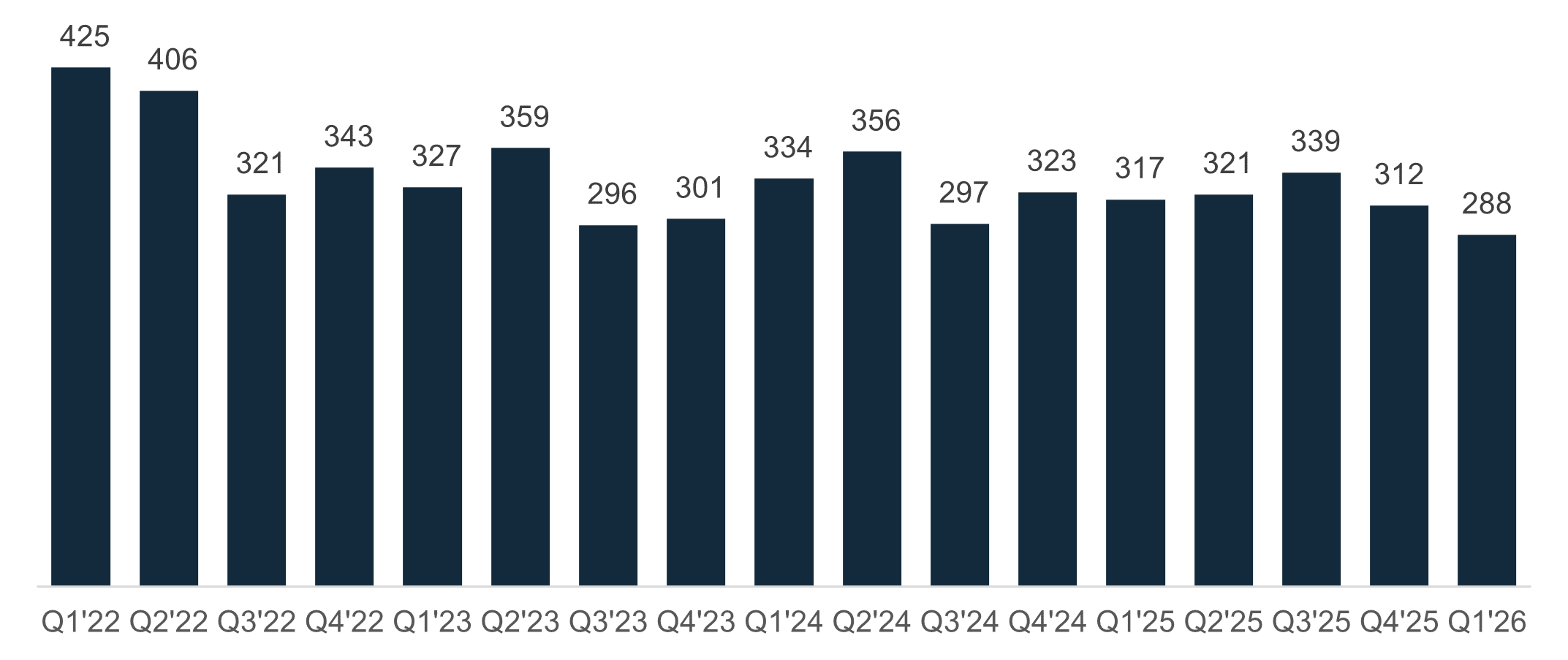

Over the longer-term, Canadian M&A transaction activity has been fairly consistent since 2023, with ~300 announced transactions each quarter.

Canadian M&A Transactions by Quarter

Source: S&P Capital IQ

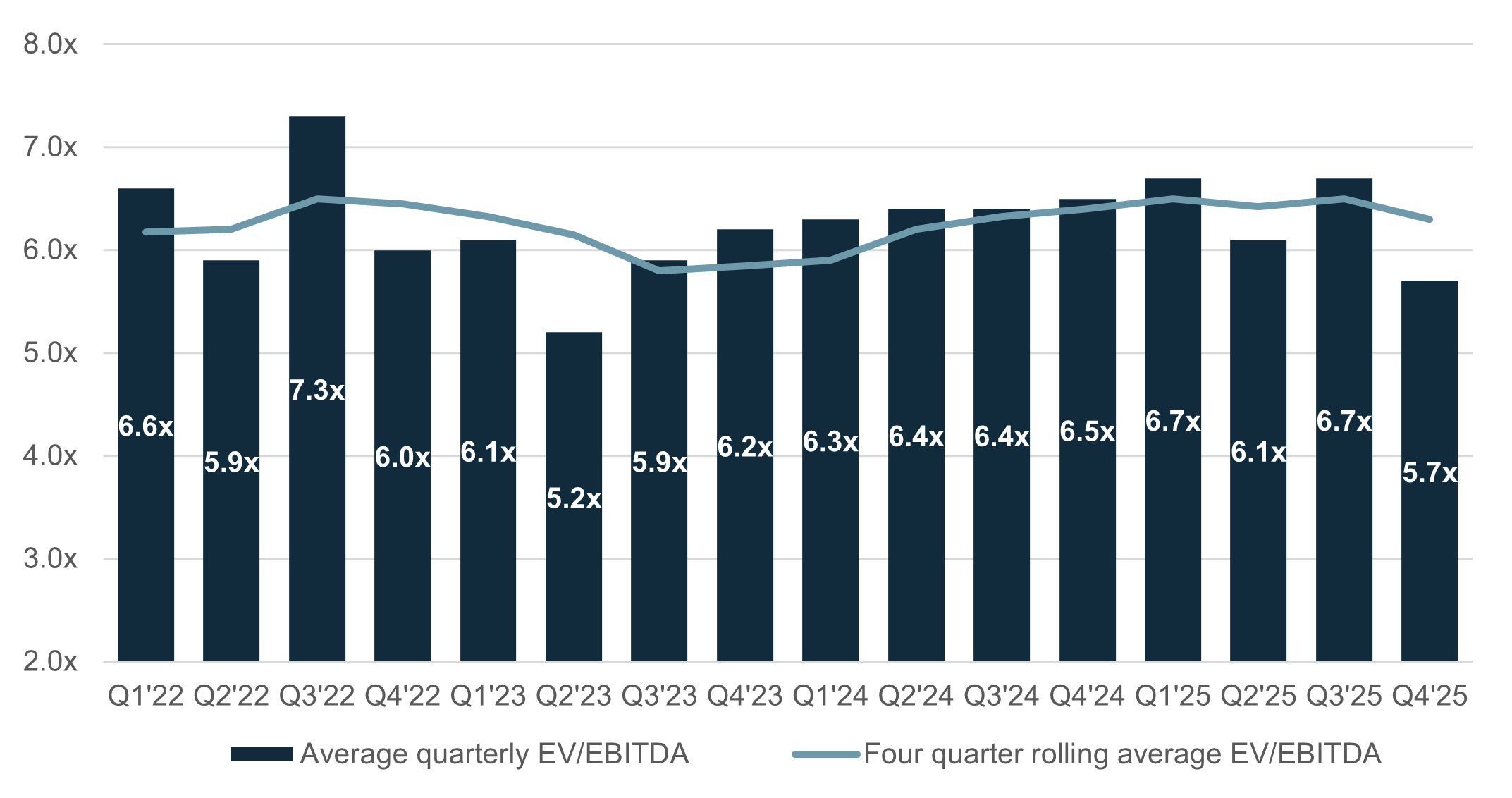

After a slight upward trend since mid-2023, valuation multiples for North American private equity transactions in the US$10-25M range declined in Q4-25. We don’t expect that data from just one quarter reflects a meaningful trend, and we’re confident that the average continues to be in the 6.0x to 6.5x TEV / EBITDA range.

Average Enterprise Value / EBITDA for Private Equity Transactions (US$10-25mm)

Source: GF Data

For business owners contemplating a transition in the next 12–24 months, current conditions present a window of relative stability. Early preparation around financial readiness, tax planning, and buyer positioning continues to be a key driver of successful outcomes.

News & Events

In Q1, the Fort Capital SMB team was active at the ACG WestConnect conference and other industry events. Looking ahead to Q2, we’ll be presenting at Business Transitions Forum Alberta, CBV Institute M&A Update, Fort Capital’s ‘Exit Planning Essentials’ seminar with MacKay CEO Forums, and Clark Wilson’s ‘How to Buy or Sell a Business’ seminar.